Middle East AI Investment Surge: AWS Saudi Arabia and the Race for Regional AI Dominance

Academic References

Balland, P. A., Boschma, R., & Crespo, J. (2022). Regional diversification and smart specialization: towards a new framework for evaluating policy strategies. Cambridge Journal of Regions, Economy and Society. doi:10.1093/cjres/rsab032

Corea, F. (2019). An Introduction to Data: Everything You Need to Know About AI, Big Data and Data Science. Springer. doi:10.1007/978-3-030-04468-8

Cen, Y., Gan, Q., et al. (2023). Cogdl: A comprehensive library for graph deep learning. ACM Transactions on Knowledge Discovery from Data. arXiv:2103.00959

Abstract

The Middle East has emerged as one of the world’s most contested AI infrastructure battlegrounds, with Gulf states deploying trillions in sovereign wealth to position themselves as neutral nodes in an increasingly fragmented global AI order. Amazon Web Services’ $5.3 billion Saudi Arabia cloud region—augmented by an additional $5 billion AI Zone built in partnership with HUMAIN, a Public Investment Fund-backed national AI champion—represents the largest single-market AI infrastructure commitment in the region’s history. Microsoft has pledged $15.2 billion to the UAE through 2029, while Abu Dhabi’s G42 and Saudi Arabia’s HUMAIN race to become sovereign AI platforms capable of serving both US and Chinese technology ecosystems simultaneously. This article examines the investment economics, geopolitical logic, and emerging risk calculus of the Middle East AI surge—including the structural vulnerabilities exposed by the March 2026 escalation of US-Iran military conflict, which now threatens the very infrastructure corridor that Big Tech has spent years constructing.

The Strategic Context: Sovereign Wealth Meets AI Infrastructure

The Gulf Cooperation Council states collectively command approximately $5 trillion in sovereign wealth, a capital reservoir that dwarfs the GDP of most nations and positions Saudi Arabia and the UAE as credible counterweights to both US and Chinese AI infrastructure dominance. This concentration of capital, combined with strategic geographic positioning at the intersection of Europe, Asia, and Africa, has made the Gulf a primary target for technology firms seeking to expand AI infrastructure beyond traditional Western markets.

Saudi Arabia’s Vision 2030 program provides the institutional scaffold for this transformation. Originally conceived as an economic diversification strategy to reduce hydrocarbon dependency, Vision 2030 has evolved into one of the world’s most aggressive sovereign AI build-out programs. The Saudi National AI Strategy targets GDP contribution from AI of up to $135.2 billion by 2030, with the kingdom’s data center market projected to grow from $1.33 billion in 2024 to $3.9 billion by 2030.

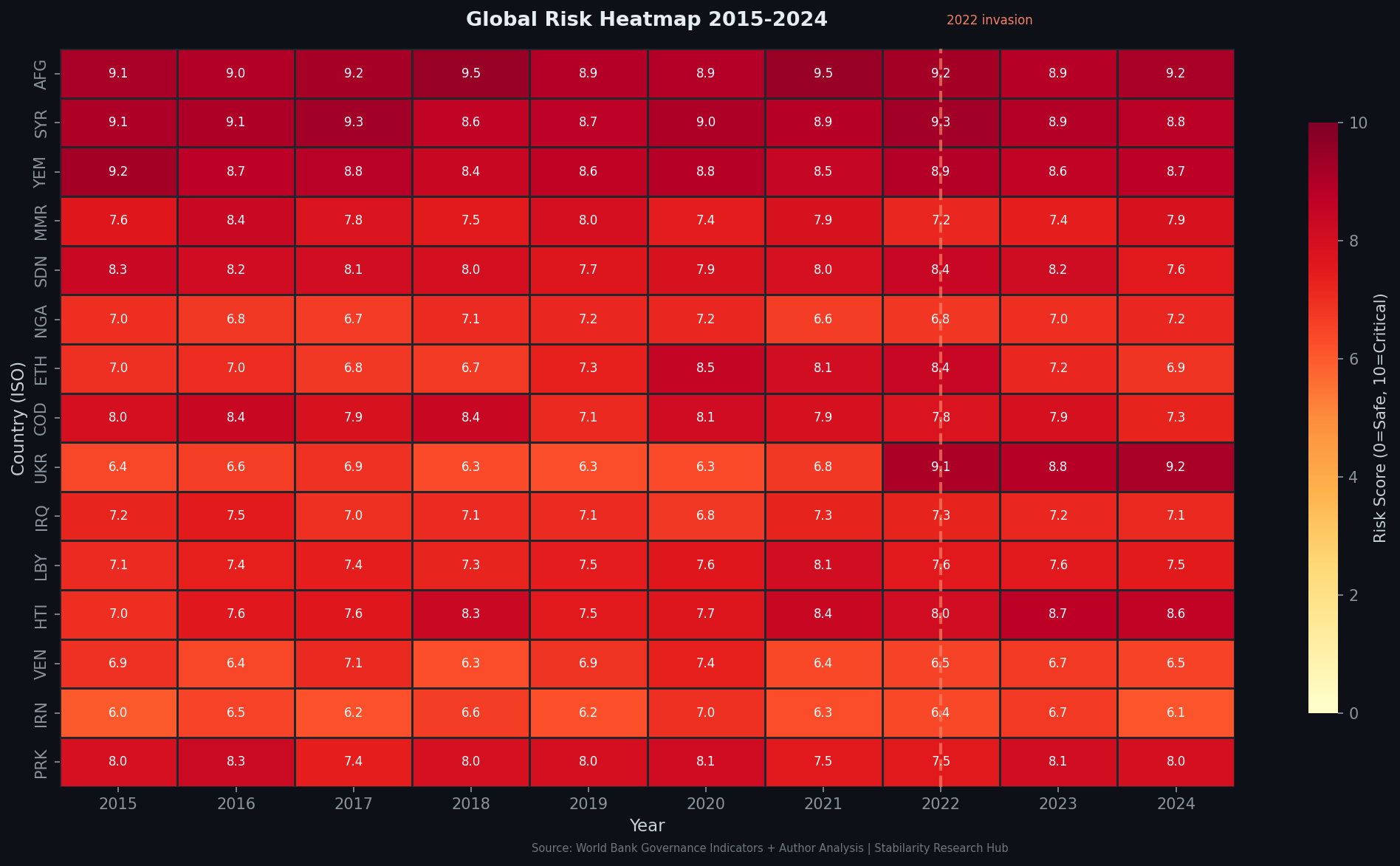

Figure 1: Geopolitical risk heatmap showing concentration of AI infrastructure investment in Gulf states versus conflict exposure zones (Source: Stabilarity GRI Model)

The United Arab Emirates has pursued a parallel but distinct strategy, leveraging its position as a global financial hub and diplomatic neutral zone to attract technology investment at a pace that has surprised even optimistic projections. The UAE’s G42, backed by Abu Dhabi state investment vehicles Mubadala and MGX, has become the regional anchor for Western technology partnerships—securing Microsoft’s equity stake, enabling NVIDIA chip deployments, and positioning Abu Dhabi as a potential home for frontier AI models serving markets that neither the US nor China can directly access without political complication.

AWS and HUMAIN: Anatomy of a $10 Billion AI Bet

The AWS Saudi Arabia investment thesis unfolds in two distinct tranches that, taken together, represent a structural commitment of extraordinary depth. The first tranche—a cloud infrastructure region comprising three Availability Zones, announced in early 2025 with $5.3 billion in committed capital—follows AWS’s established pattern of building enterprise-grade cloud regions in markets with significant sovereign cloud demand. The Saudi region was positioned to serve the kingdom’s public sector modernization agenda, including healthcare digitization, financial services transformation, and government data localization requirements under the Personal Data Protection Law.

The second tranche, announced in May 2025 through the formation of a joint structure with HUMAIN, marks a qualitative departure from standard cloud infrastructure economics. HUMAIN—established as a wholly-owned subsidiary of Saudi Arabia’s Public Investment Fund—functions simultaneously as a national AI champion, a sovereign compute platform, and a geopolitical positioning instrument. The AWS-HUMAIN AI Zone in Riyadh, announced at the Future Investment Initiative in November 2025, will deploy up to 150,000 AI accelerators in a single purpose-built facility—a compute concentration that rivals the largest AI training clusters in the United States.

graph TD

PIF[Saudi Public Investment Fund] --> HUMAIN[HUMAIN - National AI Platform]

HUMAIN --> AWS_ZONE[AWS AI Zone Riyadh

150K AI Accelerators]

HUMAIN --> AIRTK[AirTrunk DC Campus

~$3B Phase 1]

HUMAIN --> ARAMCO[Aramco Digital

LLM Development]

AWS[Amazon Web Services] --> AWS_ZONE

AWS --> SA_REGION[AWS Saudi Arabia Region

3 Availability Zones

$5.3B]

NVIDIA --> AWS_ZONE

HUMAIN --> GOOG[Google Cloud

Partnership]

HUMAIN --> MSFT_LINK[Microsoft / Azure

Collaboration]

style PIF fill:#2a5298,color:#fff

style HUMAIN fill:#1a7a4a,color:#fff

style AWS_ZONE fill:#d4500a,color:#fff

Figure 2: HUMAIN investment architecture — PIF-backed AI ecosystem spanning cloud infrastructure, hyperscaler partnerships, and national LLM development

HUMAIN’s partnership portfolio reads like a who’s who of global AI infrastructure: NVIDIA, Microsoft, AMD, Qualcomm, AWS, Google Cloud, and Groq have all signed framework agreements. The Blackstone-backed AirTrunk data center campus deal, announced in October 2025 with an initial commitment of approximately $3 billion, adds hyperscale colocation capacity to complement HUMAIN’s owned compute. HUMAIN has also announced plans for a dual listing on Saudi and NASDAQ exchanges within four years—signaling an intent to become a publicly traded sovereign AI infrastructure platform with global capital market exposure.

The economic logic is compelling. Saudi Arabia can offer hyperscalers something no other market provides in equivalent combination: sovereign capital underwriting risk, guaranteed government procurement, abundant and increasingly low-carbon energy (through NEOM’s solar buildout), and strategic neutrality that allows the kingdom to serve clients from both sides of the US-China AI divide.

The UAE Parallel Track: Microsoft, G42, and Abu Dhabi’s $15 Billion Commitment

The UAE’s AI infrastructure surge follows a structurally similar but institutionally distinct playbook. Microsoft’s $15.2 billion commitment to the UAE spanning 2023 through 2029—driven by an expanding partnership with G42, including a $1.5 billion equity stake—represents the largest single corporate AI infrastructure commitment in the Gulf. By March 2026, Microsoft had already deployed $7.3 billion, with a further $7.9 billion planned through 2029, nearly quadrupling local data center computing capacity.

The White House’s May 2025 decision to authorize advanced semiconductor exports to the UAE for an AI campus in Abu Dhabi built by G42 marked a geopolitical inflection point. The export authorization—covering hundreds of thousands of leading-edge chips from NVIDIA—effectively granted the UAE preferential access to compute technology that remains restricted for most non-allied nations. The decision reflected a strategic judgment that G42’s US-aligned governance structure and commitment to exclude Chinese technology from its infrastructure warranted treatment equivalent to a close ally.

Figure 3: Political versus economic risk decomposition for Gulf AI infrastructure investments — showing elevated political risk premium against strong economic fundamentals (Source: Stabilarity GRI Model)

This authorization also illustrated the central strategic tension in Gulf AI investment: both Saudi Arabia and the UAE are actively courting technology partnerships with both the United States and China, a dual-alignment strategy that US policymakers have simultaneously enabled (through chip export authorizations) and constrained (through export control regimes that limit AI chip transfers to entities with Chinese technology exposure). HUMAIN’s explicit partnership list—which includes US firms but conspicuously avoids naming Chinese technology partners in official communications—reflects careful navigation of this constraint.

The Investment Race: Comparative Regional Economics

xychart-beta

title "Gulf AI Infrastructure Investment Commitments ($B) 2025-2029"

x-axis ["AWS/HUMAIN Saudi", "Microsoft UAE", "Google UAE/SA", "NVIDIA HUMAIN", "AirTrunk HUMAIN"]

y-axis "Committed Investment ($B)" 0 --> 20

bar [10.3, 15.2, 3.5, 2.0, 3.0]

Figure 4: Comparative committed investment values across major Gulf AI infrastructure programs (Sources: AWS, Microsoft, Reuters, BusinessWire, PIF)

The cumulative scale of committed investment in Gulf AI infrastructure has crossed $40 billion across announced programs as of early 2026—a figure that, while smaller than the United States’ $500 billion Stargate program, represents a density of capital deployment per capita and per square kilometer that is unprecedented outside of hyperscale data center clusters in Oregon, Virginia, and Singapore.

Saudi Arabia’s investment advantage over the UAE lies in three structural factors. First, the PIF’s capital depth ($925 billion in assets under management) allows HUMAIN to underwrite infrastructure risk at a scale no private entity can match without government backing. Second, the kingdom’s hydrocarbon revenues provide a natural hedge against the energy cost volatility that makes AI compute economics uncertain elsewhere—Saudi Arabia’s electricity costs for industrial users remain among the lowest globally. Third, Vision 2030’s mandatory AI integration across government services generates guaranteed anchor demand that derisk infrastructure investment far more reliably than open-market demand forecasts.

The UAE’s comparative advantage lies in institutional flexibility, regulatory sophistication, and its established role as a global financial and logistics hub. Abu Dhabi’s concentration of sovereign wealth—through ADIA, Mubadala, and MGX—enables rapid deal execution at the intersection of finance, technology, and geopolitics. Dubai’s DIFC and Abu Dhabi’s ADGM provide financial regulatory frameworks that attract multinational technology company regional headquarters in ways that Riyadh’s more nascent commercial infrastructure cannot yet replicate.

Geopolitical Risk Recalibration: March 2026

The escalation of US-Iran military conflict in early 2026 has introduced a risk variable that Gulf AI infrastructure investment models had largely failed to adequately price. Reuters’ March 2, 2026 analysis documented the sudden uncertainty spreading across billions in committed technology investment as US and Israeli military operations against Iranian infrastructure intensified.

The structural vulnerability is geographic and physical: Gulf data centers, regardless of their technological sophistication, remain exposed to the same kinetic and electronic warfare risks that affect all physical infrastructure in the region. Iranian ballistic missile capabilities demonstrated during 2024-2025 exchanges with Israel proved capable of reaching targets across the Gulf, while Iranian cyber capabilities—extensively documented by Mandiant and CrowdStrike threat intelligence—represent a persistent threat to operational technology systems across the region.

graph LR

subgraph "Investment Thesis"

A[Sovereign Capital Backing] --> B[Infrastructure Build-Out]

C[Energy Cost Advantage] --> B

D[US Chip Access] --> B

B --> E[Regional AI Hub]

end

subgraph "Risk Vectors — March 2026"

F[US-Iran Military Escalation] --> G[Kinetic Infrastructure Risk]

H[Iranian Cyber Capability] --> I[Digital Infrastructure Risk]

J[Strait of Hormuz Exposure] --> K[Supply Chain Disruption]

G & I & K --> L[Investment Premium Repricing]

end

E -.->|Risk Collision| L

style L fill:#8B0000,color:#fff

style E fill:#1a7a4a,color:#fff

Figure 5: Investment thesis collision with March 2026 risk vectors — structural vulnerability of Gulf AI infrastructure to regional military escalation

The US Navy’s engagement of Iranian naval vessels in the Indian Ocean in early March 2026 has extended the risk perimeter beyond the traditional Gulf theater. The Indian Ocean represents the primary maritime corridor for fiber optic cable infrastructure connecting Gulf data centers to Europe and Asia—infrastructure that forms the connectivity backbone of any regional AI hub. Damage or disruption to these cables, whether through deliberate military action or as collateral damage, would impose severe performance degradation on Gulf-hosted AI services dependent on low-latency global connectivity.

For hyperscalers like AWS and Microsoft, the risk calculus is complex. Sunk costs of $5-15 billion are already committed or partially deployed; withdrawing is not a viable option even in a deteriorating security environment. The more likely institutional response—already visible in analyst commentary following the Reuters exposé—is accelerated redundancy investment: additional connectivity routes, hardened physical security, distributed workload architecture that can reroute compute away from at-risk zones, and enhanced cyber resilience programs.

The China Factor: Dual Alignment Under Pressure

Saudi Arabia’s positioning as a potential bridge between US and Chinese AI ecosystems has been one of the most closely watched strategic dimensions of the Gulf AI surge. HUMAIN’s official partnership portfolio lists exclusively US and Western technology firms; however, Huawei has maintained a significant commercial presence in Saudi Arabia’s telecommunications infrastructure, and Chinese construction firms have been involved in NEOM and other Vision 2030 megaprojects.

Figure 6: Forecast comparison of Gulf AI infrastructure investment trajectories versus global benchmarks, showing accelerating divergence from 2025 baseline (Source: Stabilarity GRI Model)

The semiconductor export control regime administered by the US Bureau of Industry and Security creates a structural pressure point in this dual-alignment strategy. AI chip exports to entities with material Chinese technology exposure face restrictions under the Entity List and AI Diffusion Rules frameworks; HUMAIN’s ability to sustain access to NVIDIA GPUs at the scale required for its 150,000-accelerator AI Zone depends on maintaining clean separation from Chinese technology ecosystems in ways that US regulatory authorities can audit and verify.

The Middle East Institute’s analysis of Saudi AI ambition identifies this tension as a core strategic risk: if Saudi Arabia is perceived as using US-supplied AI infrastructure to serve Chinese customers or enable Chinese AI model development through back-channel arrangements, the export authorization framework underpinning the entire Gulf AI build-out could be rapidly withdrawn. The Trump administration’s approach to this dynamic—simultaneously enabling unprecedented Gulf chip access while intensifying China export controls—suggests a strategic bet that Gulf states can be effectively decoupled from Chinese AI supply chains through economic incentives rather than punitive restriction.

Economic Implications: The Regional Multiplier Effect

The direct investment figures—$5.3 billion for AWS Saudi Arabia, $10+ billion through HUMAIN, $15.2 billion from Microsoft in the UAE—understate the regional economic impact through multiplier effects. Data center construction, power infrastructure buildout, fiber connectivity expansion, and skilled workforce development collectively generate economic activity that exceeds the primary investment by a factor of 2-4x in comparable international cases.

Saudi Arabia’s data center market growth projection—from $1.33 billion in 2024 to $3.9 billion by 2030—implies a compound annual growth rate of approximately 19.7%, well above global data center market averages and broadly consistent with accelerating AI workload demand. The kingdom has also committed to developing domestic AI talent through the National Program for Artificial Intelligence, which targets training 20,000 AI specialists and establishing 30 AI research centers by 2030.

The HUMAIN IPO trajectory—targeting dual listing on Saudi Exchange (Tadawul) and NASDAQ within four years—represents a novel financial instrument: a sovereign AI infrastructure platform that combines public capital market liquidity with implicit government guarantee structures. If successful, it would establish a template for sovereign AI monetization that other Gulf states and emerging market governments could replicate, fundamentally altering the global AI infrastructure investment landscape.

Forward Outlook: Three Scenarios for 2026-2028

Scenario 1: Managed Escalation, Resilient Investment (probability ~45%) US-Iran conflict remains below the threshold of direct Gulf state involvement. Saudi Arabia and UAE AI infrastructure investments proceed on schedule, with hyperscalers absorbing elevated political risk premiums through insurance programs and redundancy investments. HUMAIN’s AI Zone reaches operational capacity by late 2026, establishing the Gulf as a viable alternative compute region for Asian and African enterprises seeking non-US-controlled AI infrastructure.

Scenario 2: Escalation Spillover, Investment Pause (probability ~35%) Regional military escalation draws Gulf states into the US-Iran conflict, triggering force majeure clauses in major infrastructure contracts and delaying AWS Saudi Arabia region launch. Insurance premiums for Gulf data center assets rise sharply; Microsoft accelerates UAE data localization but reduces new capital commitments pending security assessment. HUMAIN IPO timeline shifts to 2030+.

Scenario 3: US Chip Access Withdrawal, Chinese Pivot (probability ~20%) Saudi Arabia’s dual-alignment strategy is deemed incompatible with US export control requirements; NVIDIA chip supply to HUMAIN is restricted or conditioned on governance requirements that PIF cannot accept. Saudi Arabia accelerates engagement with Chinese AI infrastructure providers—Huawei, Baidu, and Alibaba Cloud—as strategic hedge, triggering a bifurcation of Gulf AI infrastructure along US-China alliance lines.

Conclusion: The Gulf as a Mirror of Global AI Fragmentation

The Middle East AI investment surge is simultaneously a story about economic transformation, sovereign technology strategy, and the deepening fragmentation of the global AI order. Gulf states have identified—correctly—that the transition from hydrocarbon-dependent economies to knowledge-intensive economies requires not just financial capital but computational capital: the AI infrastructure that will underpin every economic sector by the 2030s.

AWS’s $10+ billion Saudi Arabia commitment, Microsoft’s $15.2 billion UAE program, and the emergence of HUMAIN and G42 as sovereign AI platforms are not merely commercial investments—they are geopolitical bets on which nations will be positioned to influence AI governance, standard-setting, and technology access in the decade ahead. The March 2026 US-Iran escalation has introduced a stress test that these investments have not yet faced at operational scale; the outcome of that test will shape investment appetites, risk frameworks, and strategic alignments across the global AI infrastructure landscape for years to come.

The central paradox of Gulf AI investment remains unresolved: the same geographic neutrality that makes the region attractive as an AI hub also places it within range of a conflict dynamic that neither the Gulf states nor their hyperscaler partners fully control. Managing that paradox—through redundancy, diplomacy, and careful alignment management—will define the strategic competence of both Gulf sovereign AI platforms and the global technology companies that have staked billions on their success.

Academic References

Balland, P. A., Boschma, R., & Crespo, J. (2022). Regional diversification and smart specialization: towards a new framework for evaluating policy strategies. Cambridge Journal of Regions, Economy and Society. doi:10.1093/cjres/rsab032

Corea, F. (2019). An Introduction to Data: Everything You Need to Know About AI, Big Data and Data Science. Springer. doi:10.1007/978-3-030-04468-8

Cen, Y., Gan, Q., et al. (2023). Cogdl: A comprehensive library for graph deep learning. ACM Transactions on Knowledge Discovery from Data. arXiv:2103.00959

Ivchenko, O. (2026). Middle East AI Investment Surge: AWS Saudi Arabia and the Race for Regional AI Dominance. Stabilarity Geopolitical Risk Intelligence Series. https://hub.stabilarity.com

Sources: Reuters (March 2, 2026), Amazon/AWS official announcements, Microsoft UAE investment disclosures, PIF/HUMAIN portfolio documentation, BusinessWire (November 2025), Middle East Institute, Digital Bricks AI State of AI Middle East 2025, Crowell & Moring LLP geopolitical analysis.